Post 4 in the “How to Get Started Managing Your Personal Finances” Series

Why It Matters

Once you’ve built your emergency fund and made progress on paying down debt, the next step is creating a savings plan that reflects your values, goals, and lifestyle. Saving money isn’t just about putting cash aside—it’s about deciding what kind of future you want and building the habits that will get you there.

The key is to make saving feel personal, intentional, and rewarding.

Step 1: Get Clear on What You’re Saving For

Think beyond “I should save.” Ask yourself:

- What do I want my life to look like in 1 year? 5 years? 10 years?

- How long do I want to work?

- Do I want more flexibility in my job? More travel? A bigger home? Less stress?

- What do I want to be prepared for—emergencies, retirement, kids’ college, a dream vacation?

Write down your goals and bucket them into short-term (within 1 year), medium-term (1–5 years), and long-term (5+ years).

Retirement may feel far off, but the earlier you start, the easier it is to build a strong foundation.

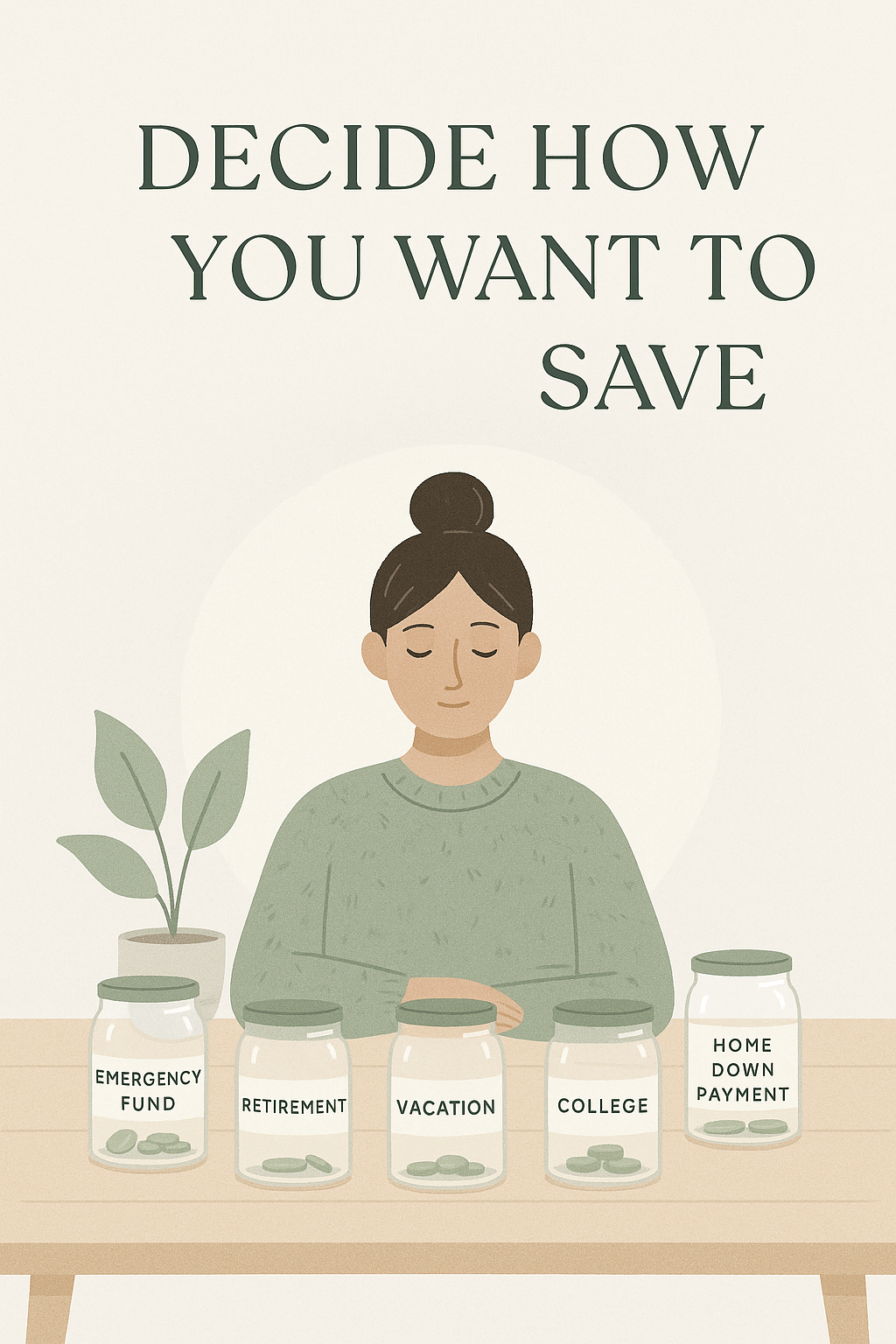

Step 2: Build Your Savings Buckets

Not all savings are created equal. Consider setting up separate savings “buckets” or sub-accounts for:

- Emergency Fund (if not already complete)

- Retirement (401(k), Roth IRA, or Traditional IRA)

- Medical Expenses (HSA if your plan qualifies)

- Home Repairs or Down Payment

- Vacation Fund

- Car Replacement

- Big Dreams or Future Projects

- Children’s college fund (529)

Prioritize these based on your goals. Naming these accounts makes your goals feel more real. You’re not just saving—you’re actively designing your life.

Step 3: Calculate How Much You Need to Save

Clarity creates motivation. For each goal, calculate:

- How much you need

- When you want to reach it

- Your monthly savings target

Example:

You want to buy a $300,000 house with a 20% down payment ($60,000) in two years. That’s $2,500/month.

If that number feels too high:

- Look at your spending—can you reduce costs like eating out?

- Find ways to increase income—can you babysit, pet sit, or freelance?

- Reevaluate your timeline or goal—maybe you lower the down payment to 10% ($30,000), reducing your target to $1,250/month.

In some cases, a higher mortgage with PMI may still cost less than rent. If so, you can work on paying down the extra mortgage principal after buying the home to remove PMI.

For retirement, aim to contribute at least enough to get your employer match. As your income grows, increase your contributions. If early retirement is your goal, work backward from your desired retirement age and calculate what you’ll need to save each year.

Clear goals help you stay focused—and avoid frustration. Saving $25/month won’t get you to a $60,000 goal in two years, and unrealistic plans can cause you to give up.

Step 4: Choose the Right Tools

Where you keep your savings matters:

- High-yield savings accounts: Ideal for your emergency fund and short-term goals

- Money market accounts: Great for medium-term savings like home repairs or car funds

- Certificates of Deposit (CDs): Useful if you won’t need the money for a fixed time

- Retirement accounts: Use tax-advantaged accounts like a 401(k), Roth IRA, or Traditional IRA for long-term investing

- Investment accounts: Consider for long-term goals beyond retirement, like generational wealth or college savings

Every dollar should have a purpose—and a smart place to grow.

Step 5: Keep Checking In

Your savings plan should grow and evolve with you. Review it every few months:

- Are your goals still aligned with your values?

- Do you need to shift more money toward a new priority?

- Can you increase your contributions, especially to retirement?

The earlier and more consistently you save for retirement, the more options you give your future self.

Reflection Prompt:

What’s one thing you want to save for that would make your life feel more meaningful, less stressful, or more free in the future?

Leave a comment